"Volatility is terrific. What we don't want is the permanent loss" Wally Weitz

As liquidity continues to boost the US indices such as the S&P and the Nasdaq with fund flows vs. fundamentals, what will happen in the second half of 2020 in terms of performance and volatility?

Larry Jones has been managing equity, fixed income, commodity and currency related strategies since 1988, as an asset allocator and a manager of direct trading of derivatives in stock indices (S&P, FTSE, DAX, ESTX, Nikkei, Hang Seng) as well as bonds, gold, silver, oil, natural gas, and agricultural products. His full bio and track record is below:

Managing Volatility Interview with Larry Jones

AV: Tell us about your background and how you managed the optional vol strategy during GFC?

LJ: I began trading options for investment banks in 1988. Most options traders tend to just buy options to suit their directional view. As a result, about 80% of them lose money. This is the result of two main factors: 1. Options buyers tend to follow a trend with the inherent risk that they buy exposure to a market after some or most of the trend has played out. In the middle or late stages of a trend, the reported fundamentals are generally positive; buyers of a trend when the headlines are positive usually have missed the best entry point. 2. Options are expensive; over a range of markets, the implied volatilities of options are on average about two vol points higher than realized volatility. Therefore, the buyers of outright options are overpaying versus theoretical value most of the time. Early on I developed techniques to mitigate both of these factors. During 15 years at investment banks, I managed OTC and exchange traded options on single equities, equity indices, government bonds, STIR, fx pairs, EM bonds and commodities.

In early 2008, I launched a Tactical Overlay product to hedge market risk. The product was designed to provide a hedge to equity risk (and the beta to equity inherent in portfolios of hedge funds). The instruments used were options on stock indices, primarily the S&P 500 Index. The product invested in put spreads, butterflies and condors; it did not invest in outright options. The product ran from June 2008 through March 2009 and returned more than 100%.

AV: How does the managing volatility strategy work in this current environment with QE infinity and massive retail flows and what asset class does the strategy balance the return per unit of risk the best?

LJ: The strategy is a series of techniques. The objectives of any option combination are to: 1. ensure the downside is limited; 2. express a view in a manner that is superior to that of simply buying an outright option - superior in terms of avoiding premium erosion and maximizing potential return per unit of risk.

The current environment can be classed as high vol – the VIX at 27 is much higher than its long- term average. A high vol environment produces many opportunities; when constructing combinations there are always cheaper options to buy and more expensive options to sell. A high vol environment tilts the probabilities in favour of more complex combinations such as condors. This is because the sale of further out of the money expensive options sharply reduces the cost of outright options. A high vol environment also produces more differentiated entry points. By contrast a low vol environment would tilt the probability toward simpler combinations such as vertical spreads.

The effect of QE infinity may prove to be bullish for risk assets in the short to medium term as excess monetary and fiscal stimulus eventually finds its way into asset classes. To the extent that fiscal irresponsibility ultimately will lead to inflation, this could be bullish for Gold or other “hedges” as the market anticipates inflation. From the perspective of positioning in options combinations, the most favoured assets are those where there is substantial skew in the implied volatility curves. There are substantial downside skews in all stock indices and upside skews in many commodities such as Gold.

AV: Have passive investing, rules based strategies via algorithms permanently distorted price discovery of assets as the implied volatility is exaggerated? How does the Managing Volatility Strategy work in this environment?

LJ: It is more accurate to say that passive investing temporarily distorts price discovery. For example, strong inflows into or outflows from markets can cause prices to overshoot. To the extent that the resulting price moves are larger than those which would be justified by changes in fundamentals, this creates excess volatility which is good for a strategy focused on buying low and selling high. This is true whether the excess flows come from unsophisticated investors into ETFs, trend signals from CTAs or allocation signals from risk parity programmes.

AV: Is it better to be Long Volatility in this cycle vs. Long Tail Risk Positions?

LJ: Depending on definitions, it is not recommended to be either “Long Volatility” or “Long Tail Risk.”

“Long Volatility” usually denotes being long (or net long) of options in outright directional positions or in straddles. These strategies suffer from the problems that 1. the outright options are expensive and 2. the positions can suffer excessive premium erosion. Long Vol strategies can pay off very well but perhaps only do so once or twice per decade with the benefit of hindsight. The history of Long Vol strategies is that investors get bored with the bleeding; they redeem and do not have the protection in place when markets turn down.

In almost all environments it is better to position in “Managed Vol” techniques where there is a high degree of focus on 1. Identifying cheap versus expensive options; 2. mitigating against premium erosion; and 3. generating the potential for an outsized payoff in non-extreme market outcomes.

“Long Tail Risk” usually denotes owning protection in the form of puts below the money. If the puts are on stock indices, they are doubly expensive as the put skew (implied volatilities of put options increase as the puts are further out of the money) is on top of the inherent expensiveness of options (implied vols are usually higher than realized vols).

Here again, in almost all environments it is better to position in a “Managed Vol” solution which has the capacity to sharply reduce the cost of outright options, thereby saving costs and living to fight another day in the scenario of flat or rising markets. Managed vol positions can be constructed which do not suffer premium erosion in a sideways market and still capture profits in a falling market.

AV: Besides in a core satellite portfolio or as a tactical overlay to a multi-asset class portfolio, how can the Managing Vol Strategy add alpha?

LJ: The techniques can be utilized to provide an “overlay” or, more precisely, a profile of negative correlation to equity markets in a smarter way than simply selling futures or buying outright put options. This could be highly complementary to a multi-asset portfolio which has a residual beta of, say, 30% to 60% to equity markets. The beta of any portfolio can be estimated and a programme can be designed to accomplish the desired overlay function.

Or, the techniques can be used to efficiently capture upside. For example, if the judicious use of equity call options can limit risk to say, 2%, and still capture the upside of an equity market, this superior risk/reward profile is correctly called “Alpha.” The Call Ratio Index has an attractive profile from this perspective.

Or, a programme can capture potential returns from multiple asset classes, opportunistically allocating to options positions in equity, fixed income, fx and commodities. The benchmark can be Absolute Return and any attractive Sharpe ratio or Sortino ratio produced would be “Alpha.”

As CIO of CURA & SENECTUS INVESTMENT AG, Mr. Jones oversees portfolio management of fund products across all asset classes as well as derivatives trading. As CEO of Michaelson Capital Partners, New York, Mr. Jones oversaw debt and equity investment into clean energy, nanotechnology, digital ledger and waste management technology companies.

As Head of Portfolio Management at AXA INVESTMENT MANAGERS, he oversaw a $9BN portfolio across all equity, fixed income and alternative strategies. Under his leadership, AXA IM multi-strategy portfolios won five industry awards for risk adjusted returns. As CIO of NEDBANK, Mr. Jones managed multi-strategy portfolios and overlay strategies. The tactical overlay portfolio deployed index put combinations and produced outstanding profits during the 2007-2009 bear market.

At UNITED FINANCIAL OF JAPAN, he ran a trading desk covering a full range of equity and fixed income derivatives. Substantial profits were earned using option combinations in the bear market of 2001-2002. At WEST DEUTSCHE LANDESBANK, Mr., Jones was a market maker in emerging market bond options and managed equity and fixed income derivative portfolios. At BANQUE ARABE INTERNATIONALE D’INVESTISSEMENT, he managed portfolios of equity, convertible, commodity and fx derivatives. At ABU DHABI INVESTMENT AUTHORITY, he was responsible for European equity derivatives.

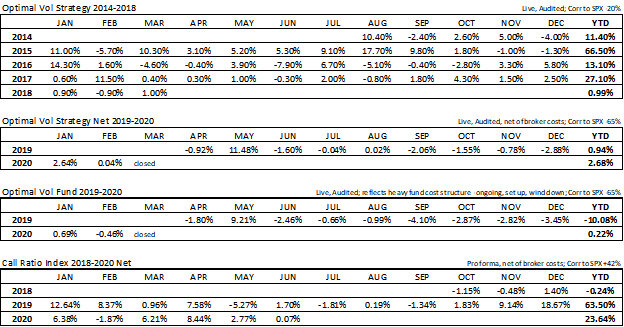

Track Record Data

Additionally, Mr. Jones managed the Tactical Overlay strategy from June 2008 to March 2009. The portfolio was positioned in S&P put combinations and generated more than 100% return. Correlation to SPX was – 65%.